I

Introduction

Evaluating a Social Impact Bond requires a dual-track analytical methodology that simultaneously evaluates social impact and financial sustainability. In the United States, this assessment is more than just an accounting exercise. Rather, it is a high-stakes scientific project that frequently uses sophisticated cost-benefit analyses and randomized controlled trials (RCTs) to decide whether to release millions of dollars in taxpayer funds to investors. There are a few of the landmark U.S. projects that can be examined to understand the complex approaches used to value social change. Some of these include the nation’s first attempt at Rikers Island, the complex, ten-year juvenile justice initiative in Massachusetts, and the contentious preschool expansion in Utah.

II

Critical Statistics on Social Impact Bond (SIB)

In this section, we will consider critical statistics on social impact bonds.

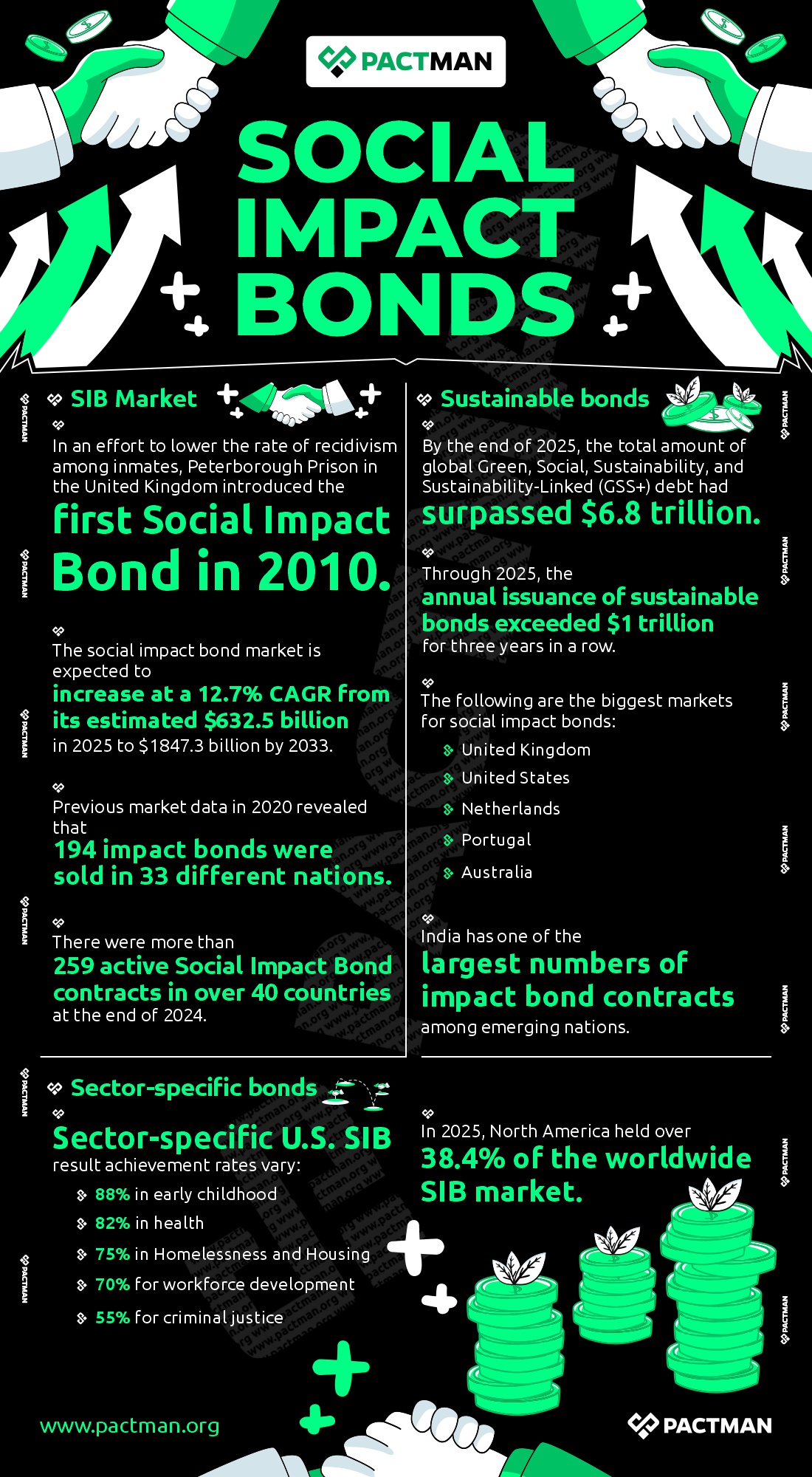

1. SIB Market

In an effort to lower the rate of recidivism among inmates, Peterborough Prison in the United Kingdom introduced the first Social Impact Bond in 2010.

The social impact bond market is expected to increase at a 12.7% CAGR from its estimated $632.5 billion in 2025 to $1847.3 billion by 2033. Previous market data in 2020 revealed that 194 impact bonds were sold in 33 different nations. Also, there were more than 250 active Social Impact Bond contracts in over 40 countries by the end of 2024.

2. Sustainable bonds

By the end of 2025, the total amount of global Green, Social, Sustainability, and Sustainability-Linked (GSS+) debt had surpassed $6.8 trillion. Through 2025, the annual issuance of sustainable bonds exceeded $1 trillion for three years in a row.

Also, by the end of 2025, there were over $827 billion in outstanding social bonds worldwide.

The following are the biggest markets for social impact bonds:

- United Kingdom

- United States

- Netherlands

- Portugal

- Australia

India has one of the largest numbers of impact bond contracts among emerging nations.

3. Sector-specific bonds

Sector-specific U.S. SIB result achievement rates vary:

- 88% in early childhood

- 82% in health

- 75% in Homelessness and Housing

- 70% for workforce development

- 55% for criminal justice

In 2025, North America held over 38.4% of the worldwide SIB market.

III

Frameworks for Financial Assessment: Determining Risk and Return

When evaluating a social impact bond, investors weigh the social risk of the intervention against the opportunity for payback. In contrast to standard bonds, which pay interest based on the borrower’s creditworthiness, the yield on a social impact bond is dependent on the target population’s behaviour. This creates a performance risk that demands more due diligence.

a. The Capital Stack and Risk Mitigation

To account for varying investor risk appetites, social impact bonds in the US often employ a tiered capital stack. Included in this framework are commercial capital, philanthropic first-loss gifts, and junior debt. The financial framework of the Massachusetts Juvenile Justice Pay for Success Initiative was created to safeguard senior investors while enabling charitable partners to assume more risk in order to demonstrate the model’s feasibility.

| Funding Tier | Investor Type | Amount | Repayment Priority |

| Senior Loan | Goldman Sachs Social Impact Fund | $8,000,000 | First priority; base interest rate ~5%. |

| Junior Loan | Kresge Foundation & Living Cities | $2,660,000 | Second priority; base interest rate ~2%. |

| Grants | Arnold Foundation, New Profit, Boston Foundation | $5,450,000 | Used for evaluation costs and first-loss protection. |

| Deferred Fees | Roca, Inc. & Third Sector Capital | ~$3,300,000 | Paid only after all other investors are made whole. |

In this context, calculating the success payment triggers is required for evaluating the financial return. This minimum improvement required serves as a financial evaluation threshold, guaranteeing that the government does not pay for outcomes that could be attributed to random chance or modest seasonal variations.

b. Cost-benefit analysis and public value considerations

Secondly, the government uses cost-benefit analysis (CBA) to evaluate budgetary decisions. The objective is to see if the success payments provided to investors are less than the avoided costs created by the social program. This is sometimes described in terms of financial savings, such as lowering the demand for prison beds, homeless shelters, or special education programs.

A rigorous social cost-benefit analysis quantifies intangible outcomes like better quality of life and community safety, even if they do not directly result in government savings. However, in the U.S. social impact bond market, the emphasis has traditionally been on tangible consequences that directly influence government balance sheets, as these are easier to convert into payment formulae.

IV

Social Evaluation Frameworks: The Science of Impact Attribution

Evaluating a social impact bond requires distinguishing between the program’s impact and external influences, which can be tough. In the United States, the “gold standard” for this evaluation is the Randomized Controlled Trial (RCT).

a. Randomized Controlled Trials & Counterfactual Risk

A social impact bond evaluation aims to handle counterfactual risk. This refers to the possibility that social benefits would have occurred regardless of economic trends, policy changes, or time. In an RCT, eligible participants are randomly allocated to either a treatment group (who get the intervention) or a control group (who do not).

The independent evaluator evaluates the outcomes of both groups to establish the program’s net impact. This approach guarantees that investors are solely compensated for the value that the service provider truly adds.

b. Alternatives to the Gold Standard: Administrative Data and DID

RCTs are not always practical or desired, despite their strong scientific credibility. They may be costly, morally challenging, and slow to yield results. As a result, several U.S. initiatives adopt alternate techniques, including historical baseline comparisons or Difference-in-Differences (DID).

The DID method contrasts the participants’ pre- and post-program outcomes with those of a comparable, non-participating group within the same time frame. Both RCT and DID techniques were applied in the Massachusetts Juvenile Justice project’s final evaluation in 2024. It’s interesting to note that the DID estimations indicated a stronger positive influence, whilst the RCT produced statistically equivocal results. This illustrates how the evaluation methodology selection can significantly change how well a program is perceived.

V

Challenges in Assessing Social Impact Bonds

The happenings in the United States have exposed several structural issues that make assessing social and financial rewards more difficult.

1. The conflict between Epistemic Idealism and Market Pragmatism

There is a heated argument between those who support the gold standard of RCTs (the epistemic idealists) and those who contend that such rigour prevents the market from expanding (the market pragmatists). The RCT model’s detractors liken it to a Maserati or a beautiful little jewel box, very valuable but possibly superfluous when a more useful Camry (like administrative data tracking) would be sufficient to demonstrate a program’s effectiveness.

Smaller NGOs are especially affected by this conflict since they cannot afford the intensity of a multi-year RCT. In order to properly assess a Social Impact Bond, a technique that is proportionate to the investment amount and the body of current evidence must be used.

2. Execution Risk and Deficits in Referrals

Even if a program is providing high-quality services, an evaluation may fail, as seen in the Massachusetts case. Execution risk is the possibility that the project will not adhere to the intended evaluation procedure. This frequently shows up as a referral shortfall, in which the government is unable to enroll enough people in the program to provide a sample that is statistically significant.

Therefore, continuous performance management by the intermediary is necessary to assess a bond’s progress. In order to avoid a complete evaluation failure at the conclusion of the five to seven-year period, they must continuously check referral rates, participant retention, and data quality.

VI

Metrics Development: Career Impact Links

Career Impact Bonds have emerged as a result of the lessons learned from Social Impact Bonds. These bonds streamline the evaluation process by concentrating on one distinct financial metric: individual income.

Under a Career Impact Bond, students receive training at no cost up front and only have to pay back the tuition if they land a job that pays more than a certain living wage criterion (such as $40,000). The evaluation is simple:

- Social Return: Is the individual making more money than they were previously?

- Financial Return: Does the participant fulfil their income-based obligations?

Compared to conventional Social Impact Bonds, this model makes the evaluation far less costly and more scalable by eliminating the requirement for a complex counterfactual or a government outcome payer.

Conclusion

The US experience over the last decade has shown that, while these bonds are not a silver bullet for social ills, they can provide a powerful instrument for data-driven policymaking. The evaluation’s worth as a social impact bond lies not only in the success payment but also in the learning it offers. Even failures such as Rikers Island or Massachusetts’ unclear results provide high-quality evidence that allows governments to stop subsidising unproductive programs and divert resources to what genuinely works.

As the U.S. social impact bond market evolves, the shift toward market pragmatism will most certainly result in more standardized measurements and integrated data systems. This, in turn, will make evaluating financial and social returns an important and normal component of 21st-century social service delivery.