I

The Moral Development of American Capital and Its Historical Basis

Aligning financial choices with moral principles is a deeply ingrained American practice that predates the current stock market by centuries. According to the historical trajectory of socially responsible investing in the US, religious prohibition gave way to sociopolitical activity and, ultimately, a sophisticated framework for recognizing material financial hazards.

a. The Ethical and Religious Foundations

Religious organizations were the driving forces behind the first recorded examples of socially conscious capital allocation in America. One of the earliest ethical guidelines for investment and trade in the colonies was established in 1758. This was when the Quaker Philadelphia Yearly Meeting forbade its members from engaging in the slave trade. The founder of Methodism, John Wesley, mirrored this philosophy in his sermon “The Use of Money” from the 18th century. The sermon provided a clear foundation for moral economic practices.

Wesley contended that in addition to pursuing financial gain, investors need to steer clear of sectors that endanger the environment or the health of their workforce. He cited the manufacturing of chemicals and tanning as examples of industries that produce harmful externalities. Essentially, the main focus of these early initiatives was negative screening, or keeping sinful businesses like alcohol, tobacco, and gambling out of a person’s portfolio.

b. Civil Rights and the Vietnam War in the Modern Era

Also, the sociopolitical furnace of the 1960s shaped the present form of socially responsible investing. Investors started to realize during this time that their money might be used to effect both domestic and global change. The Montgomery bus boycott and the Operation Breadbasket Project in Chicago were two economic strategies used by the civil rights movement. This was spearheaded by individuals like Martin Luther King Jr. to compel businesses to confront racial inequalities.

Anti-war sentiment also increased during this time, with investors focusing on businesses like napalm manufacturer Dow Chemical, indicating that corporations involved in the military-industrial complex would suffer financial repercussions from ethical shareholders.

II

Critical Statistics on Socially Responsible Investing

In this section, we will consider critical statistics on socially responsible investing and its impact across the globe.

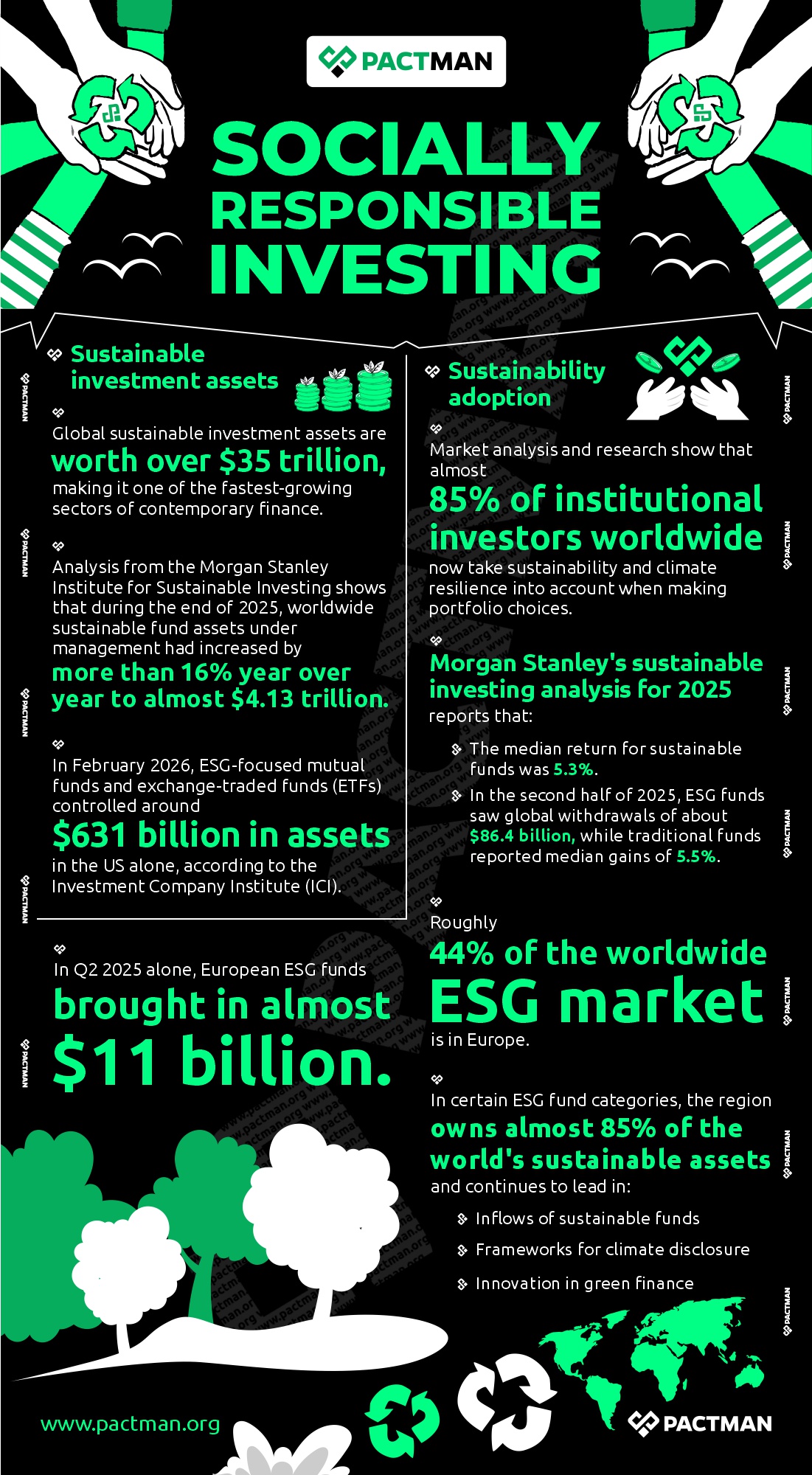

a. Sustainable investment assets

Global sustainable investment assets are worth over $35 trillion, making it one of the fastest-growing sectors of contemporary finance. Analysis from the Morgan Stanley Institute for Sustainable Investing shows that by the end of 2025, worldwide sustainable fund assets under management had increased by more than 16% year over year to almost $4.13 trillion.

In February 2026, ESG-focused mutual funds and exchange-traded funds (ETFs) controlled around $631 billion in assets in the US alone, according to the Investment Company Institute (ICI).

b. Sustainability adoption

Market analysis and research show that almost 85% of institutional investors worldwide now take sustainability and climate resilience into account when making portfolio choices. Morgan Stanley’s sustainable investing analysis for 2025 reports that:

- The median return for sustainable funds was 5.3%.

- In the second half of 2025, ESG funds saw global withdrawals of about $86.4 billion, while traditional funds reported median gains of 5.5%.

Roughly 44% of the worldwide ESG market is in Europe. In certain ESG fund categories, the region owns almost 85% of the world’s sustainable assets and continues to lead in:

- Inflows of sustainable funds

- Frameworks for climate disclosure

- Innovation in green finance

In Q2 2025 alone, European ESG funds brought in almost $11 billion.

III

Strategic Structures for Socially Responsible Investing

When assessing a business for socially responsible investing, it is necessary to comprehend the specific approach being used. From proactive impact generation to passive exclusion, investors in the U.S. market employ various strategies.

1. Negative and exclusive Screening

Investors continue to enter the market mostly through negative screening. Essentially, it entails removing specific businesses or whole sectors from a portfolio because the investor’s values are at odds with their operations. The 2025 US SIF Trends Report states that negative screening is still a fundamental instrument used by 72% of sustainable investors. Companies engaged in tobacco and e-cigarettes, problematic weapons, and fossil fuels are often excluded in the United States. However, negative screening is sometimes criticized for being reactive rather than promoting systemic organizational change. This is, although it is successful for aligning a portfolio with moral norms.

2. Positive Attitude and Top-Rated Selection

Positive tilt strategies, as opposed to negative screening, deliberately seek out businesses that outperform their industry counterparts in environmental, social, and governance (ESG) domains. For example, instead of investing in a peer firm with bad labor relations or a higher carbon intensity, an investor may decide to overweight their portfolio with a technological company like Adobe or Microsoft, which have achieved gender pay parity and made large investments in renewable energy. This best-in-class strategy is predicated on the idea that businesses with robust ESG profiles are better managed and more resilient to long-term hazards.

3. Impact and Thematic Investing

Thematic investing prioritizes specific environmental or social challenges, such as gender diversity, clean water, or alternative energy. By aiming to provide a quantifiable, favorable social or environmental impact in addition to a financial return, impact investing goes one step further. Now more than ever, impact investing is growing rapidly in the United States. 61% of sustainable investment practitioners say they use it to find solutions for equitable economic growth and energy transition.

In contrast to more general ESG approaches, impact investing requires specific statistics to verify the effectiveness of the investment. This can be the number of affordable housing units constructed, or the precise metric tons of CO2 sequestered.

4. Stewardship and Advocacy for Shareholders

Lastly, shareholder advocacy is the practice of influencing a company’s policies and actions through one’s ownership stake in the company. This is accomplished via filing shareholder resolutions, exercising proxy voting rights, and having direct conversations with corporate management. As of 2025, active stewardship policies covered about $42.7 trillion in U.S. assets, making it a powerful force in the country. Major American corporations have been effectively pressed by shareholder groups to diversify their boards of directors, report on their political expenditures, and disclose their climate risks.

IV

The Three Foundation Metrics: Environment, Society, and Governance

A company’s socially responsible investing review is usually structured on the three ESG pillars. Hence, investors can measure a company’s sustainability and ethical impact using these parameters.

a. The Environmental Pillar (E)

This pillar emphasizes a business’s responsibility to protect the environment. Now more than ever, this pillar has grown more data-driven as businesses in the US are under pressure to disclose their resource efficiency and greenhouse gas (GHG) emissions.

- Carbon Emissions (Scope 1, 2, and 3): Three categories of emissions are examined by investors.

- Scope 1: Direct emissions from sources owned by the corporation.

- Scope 2: Indirect emissions from purchased electricity.

- Scope 3: All additional indirect emissions in the value chain, such as those from suppliers or the usage of sold goods, which is frequently the biggest and most complex.

- Water Management: Water scarcity is a significant challenge, especially in the Western United States. Investors assess a company’s recycling rates, water usage, and how its operations affect nearby watersheds.

- Waste and Circularity: This refers to a business’s dedication to minimizing landfill waste as well as its accomplishments in rerouting operational waste via recycling or composting initiatives.

b. The Social Pillar (S)

This pillar looks at how a business handles its interactions with people, including its employees, clients, and the communities in which it operates.

- Human capital management: This includes employee turnover statistics, racial and gender diversity in the workforce, and training and development expenditures.

- Workplace Safety: One of the main indicators of operational health in industrial sectors is safety. Investors monitor the Lost Time Injury Rate (LTIR), which quantifies injuries resulting in missed workdays, and the Total Recordable Incident Rate (TRIR), which calculates injuries per 200,000 hours worked.

- Data Privacy and Cybersecurity: Safeguarding customer data is an essential social duty in the digital era. Failing to do so may result in significant legal risks and a decline in customer confidence.

c. The Governance Pillar (G)

Lastly, governance evaluates the internal systems of policies, procedures, and guidelines that govern how a business is run. It frequently serves as the best indicator of long-term financial stability.

- Board Independence and Diversity: To guarantee impartial monitoring, investors need an independent board of directors with a diversified background.

- Executive Compensation: Crucial evaluation criteria include whether executive compensation is in line with long-term shareholder value and whether bonuses are dependent on meeting ESG goals.

- Ethics and Transparency: This covers a company’s anti-corruption procedures, safeguards for whistleblowers, and the openness of its political contributions and lobbying.

V

Interpreting Third-Party Ratings: Sustainalytics and MSCI

Third-party rating organizations are now the gatekeepers of socially responsible investing data in the United States. This is largely because individual investors are not always able to conduct in-depth research on every investment.

A. The Industry-Related Model of MSCI ESG Ratings

With over 17,000 issuers covered, MSCI is one of the top ESG rating suppliers in the world. Because of its industry-relative methodology, businesses are evaluated based on their direct counterparts rather than a universal benchmark. Essentially, MSCI uses a letter-grade scale ranging from AAA to CCC.

- Leaders (AAA, AA): These are businesses at the forefront of their sector in terms of handling the biggest ESG opportunities and threats.

- Average (A, BBB, BB): These are classified as businesses having a varied history of risk management in comparison to their counterparts.

- Laggards (B, CCC): These are businesses that fall behind their sector as a result of high exposure and inadequate management of major ESG risks.

A crucial feature of the MSCI model is its ability to identify key issues for each industry. For instance, a utility company places a high value on carbon emissions, whereas a social media corporation places a high value on data privacy.

B. Sustainalytics by Morningstar: The Absolute Risk Model

Secondly, Sustainalytics’ emphasis on unmanaged ESG risk offers an alternative viewpoint. In contrast to the relative letter grades used by MSCI, Sustainalytics offers a numerical score on a scale of 0 to 100, where a lower number denotes less uncontrolled risk. Hence, investors can now easily compare an oil company’s ESG risk to that of a bank.

Essentially, the two-dimensional framework of Sustainalytics begins by assessing a company’s risk exposure. Afterwards, it assesses how well it manages that risk. For instance, a mining company’s ultimate unmanaged risk score may be lower than that of a peer with less exposure but inadequate management if it has top-notch safety and remediation procedures.

Conclusion

An investor should combine quantitative evaluations with qualitative analysis to assess a firm for Socially Responsible Investing in the U.S. market. By adhering to this accountability framework, investors may match their financial objectives with their personal principles. This helps to create a more equitable and sustainable global economy while identifying the businesses most likely to prosper in the next decades.